Consider the 21st century’s most ubiquitous piece of financial advice: “Can’t afford a house? Just stop buying lattes.”

Every millennial has heard some kind of variation of this myth. It’s peppered all over Twitter, dispensed on personal finance blogs, and uttered from the mouths of pundits on national television. Sometimes, “latte” is exchanged for a different millennial trope, like avocado toast.

The idea that fewer lattes could solve millennials’ financial woes has been around for more than 20 years and can be traced to one man: a financial adviser and author named David Bach.

“Are you latte-ing away your future?” Bach asked in a 1999 book. “Everyone makes enough money to become rich. What keeps us living paycheck to paycheck is that we spend more than we make on stuff we don’t need.”

In the 23 years since then, we’ve witnessed a dot-com crash, a Great Recession, a global pandemic, a housing shortage, 40-year-high inflation, and the massive growth of student debt.

Yet the latte is still a flashpoint for arguments about personal finance — a stand-in for any small luxury that could be given up to boost wealth, and a recurring subject in Bach’s 12 bestselling books.

David Bach wants you to stop buying lattes (Photo by Dominik Bindl/Getty Images; illustration by The Hustle)

“There’s this enormous attraction as a culture to it, and I don’t think any of us are above it,” Helaine Olen, a Washington Post opinion writer and author of Pound Foolish, a critique of the personal finance industry, told The Hustle. “I think we all believe it on some level.”

Perhaps it’s surprising that latte advice has proliferated when sweeping economic forces have put retirement and home ownership further out of reach for young workers.

But the latte advice exists because of these issues, springing into existence just as the idea of retirement seismically shifted, wages stagnated, and the price of a ticket to the middle class increased substantially.

When pensions died and personal finance boomed

David Bach grew up in the financial advice industry. His father ran his own planning practice, The Bach Group, as part of Dean Witter (now Morgan Stanley). In the early ’90s, when Bach was in his 20s, he joined his father’s practice.

The industry was thriving. In 1995, America had ~30k designated financial planners, a number that had increased 50% in the previous 5 years.

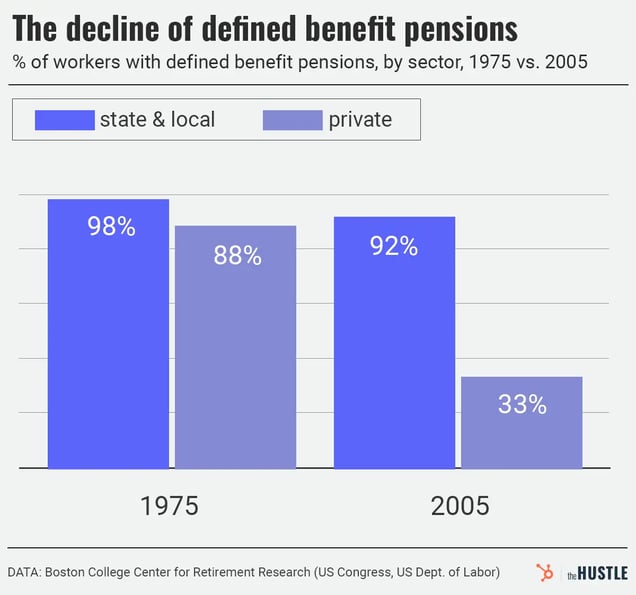

Before the personal finance boom, most people received “defined benefit” pensions. These plans required employers to guarantee and fund set payments to their workers after they retired, placing the burden of saving and investing on the employer.

Estimates vary on the amount of workers once covered by pensions. But according to data from Boston College’s Center for Retirement Research, ~88% of Americans employed in the private sector had defined benefit retirement pensions in 1975.

“Americans both needed [financial] advice less and had less reason to invest because it was assumed for most people that there would be a pension,” Olen said.

But changes were afoot:

- IRAs and 401(k)s were introduced by federal legislation in the 1970s.

- Dovetailing with a hot economy in the mid-’80s, the 401(k) replaced the defined benefit pension as the most common retirement strategy.

- By 2005, ~33% of private sector workers had defined benefit pensions, according to Boston College.

Zachary Crockett / The Hustle

The concept of retirement saving was rapidly transformed. Over time, the burden shifted from employers to employees, who had to make more savings and investment decisions on their own.

In the aftermath, financial planners and money managers became a hot commodity — as did self-help advice presented in books and on TV.

But because telling people it was important to invest earnings while not overspending could be summed up in half a sentence, catchy strategies were a requisite for making waves in the financial advice self-help sector.

Enter the latte.

Like the 401(k), the American specialty coffee scene was on the rise in the ’80s and ’90s. Local shops and massive chains like Starbucks exploded. By the mid-’90s, the specialty coffee market was estimated at $1.5B.

Specialty coffee was also instantly associated with financial decision-making — just not the way we’ve become accustomed to thinking.

Although lattes were richer in taste and price than a cup of Folgers, the beverages were seen as an alternative to excess.

Analysts hypothesized that espresso drinkers consumed lattes because they wanted to avoid nightclubs or couldn’t afford an expensive pair of jeans from Nordstrom, describing specialty coffee as “an affordable luxury in a society of downsizing incomes and expectations.”

“People are watching their money in the ’90s,” a Washington, DC coffee shop manager told the Baltimore Sun in 1994, “so coffee shops are becoming meeting places.”

The Hustle

To people who enjoyed lattes — largely urban young people and women — coffee culture was linked with fiscal responsibility.

But for older generations and suburban residents who had yet to get the first Starbucks store in their neighborhood, lattes were a mark of frivolous luxury, made famous in 1997 by opinion columnist David Brooks’s use of the phrase “latte town” to describe America’s elite bubbles.

The cultural connotations and generational divide, said Meghaan Lurtz, a professor of practice at Kansas State University who has researched the psychology of money, made the latte “an easy thing to point to.”

And plenty of people were ready to point.

Latte math doesn’t add up

“The Latte Factor” was first used by Bach in 1995, according to a trademark he later filed for the phrase.

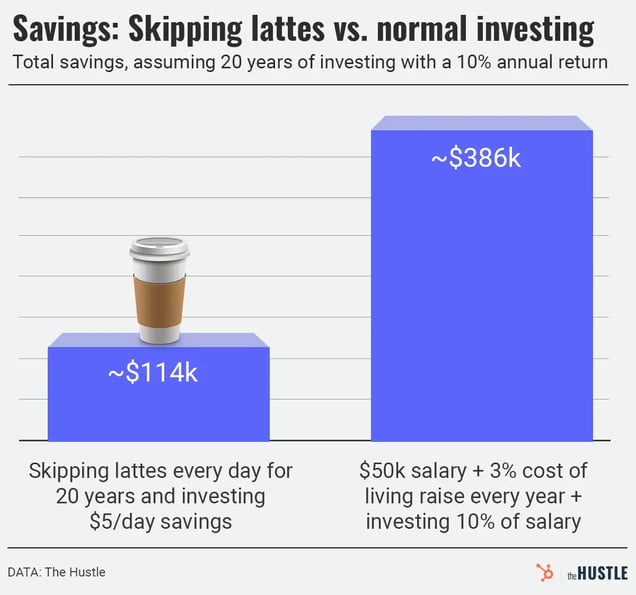

He claims he came up with it after hearing how a 23-year-old woman in one of his investment classes bought a latte every day and never had enough money to invest. He featured the advice prominently in his 1999 book Smart Women Finish Rich, calculating how this woman could one day be a multimillionaire if only she’d curb her latte habit.

- Bach estimated the cost of a latte (plus a Diet Coke and other treats) at $5/day. This placed the woman’s monthly latte expenses at $150 a month, or ~$2k/year, in Bach’s estimation.

- He told her if she skipped the latte every day and invested the $5 in stocks she would make more than $2m by the time she was 65, assuming an 11% growth rate.

Zachary Crockett / The Hustle

Bach’s formula featured some questionable math. (The annualized returns on the Dow Jones, for instance, were ~9.7% between 1949 and 1999 — not 11% — and even assuming the latter rate, Bach’s own “Latte Factor Calculator” shows that saving $5/day for 40 years wouldn’t produce anything close to $2m.)

Nonetheless, his latte advice took off.

Smart Women Finish Rich became a New York Times bestseller and Bach soon landed on The View and Oprah, emphasizing that cutting back on lattes or similar small luxuries were the key to saving enough for a good life.

He eventually created something he called the “double latte factor,” telling people to reduce spending on other items he deemed to be expensive luxuries — cellphones, gym memberships, and cable TV.

The schtick has attracted its share of critics.

“I don’t love that narrative,” Cliff Robb, faculty director of the consumer finance and personal financial planning programs at the University of Wisconsin–Madison, told The Hustle, “where we’re basically saying, ‘OK, we’ve made social safety nets weaker, we’ve taken away a lot of employee benefits that people used to get, and more stuff is on you. And you should feel bad about what you’re doing.’”

Preston Cherry, founder and president of Concurrent Financial Planning, describes the latte advice as a smart entry point to helping anyone understand how to better assess financial health.

But it works, he said, if evaluated as part of a big picture encouraging people to strive for greater abundance so they won’t have to worry about cutting back on every little thing. Without getting into the bigger picture, he said people won’t even want “to engage with [their] financial goals.”

Zachary Crockett / The Hustle

Plenty of newer personal finance experts would agree. Several business books released this year have been marketed as being “not about the latte.”

But Bach, who did not respond to multiple interview requests, has remained resolute in targeting the elimination of small expenses as a “secret” for achieving wealth even in the context of America’s economic downturns.

“Who stole the American Dream?” he asked in the 2016 edition of his book The Automatic Millionaire, noting that old approaches to saving for retirement were unsatisfactory.

Prime among his handful of solutions for attaining the dream was his most steadfast approach: “The Latte Factor®.”

What really drives the loss of wealth

The real root causes behind average people gaining or losing wealth are, of course, a bit more complex than lattes.

Going back to the time of Thorstein Veblen and “conspicuous consumption,” the answer has often been stated as being contingent on how much money you spend.

Veblen’s thoughts were updated by people like Bach, Suze Orman, and Juliet Schor, who wrote in the 1990s that “millions of us have become participants in a national culture of upscale spending.”

In 2012, Jeffrey Lundy published a dissertation questioning this long-held rhetoric, finding scant research had been conducted on what drives wealth loss and accumulation. Lundy studied patterns of spending from the US Consumer Expenditure Surveys and compared them with household wealth loss from the prior several years.

His answer? Above average discretionary spending usually didn’t lead to major changes in net wealth — but larger forces did, like divorce, job loss, high interest loans, expensive health emergencies, and being widowed.

“Americans are hard on ourselves,” Lundy told The Hustle in a message, “but it seems less of it is about frivolous spending and more about unexpected negative life circumstances.”

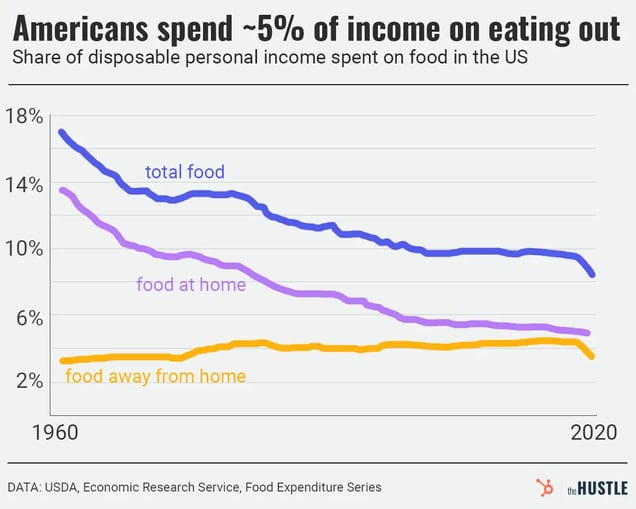

Another thing Lundy found was that Americans had spent a declining or steady amount of their total incomes on things like entertainment and recreation in the prior three decades. That was also the case with food and beverages outside the home.

We may be eating out a lot and drinking more lattes (~67m in 2017) than in the 1990s, but the share of after-tax income Americans spend on food and drink outside the home has hovered at ~4%-5% every year since 1980.

Zachary Crockett / The Hustle

Yet despite being similarly conservative with their discretionary expenditures as generations ago, Americans, aside from a change at the height of the pandemic, are not saving as much as they did in the ’80s.

To Olen, there’s a clear explanation: “People very well know how to save money. They [just] have a hard time doing it.”

In other words, the problem is a bit harder to swallow than a latte.