I recently met a guy I’ll call “Ben.”

After 7 years of “blood, sweat, and instant noodles,” Ben built his startup into an exciting enterprise. He raised a hefty round from a “top-tier” venture capital firm. And in 2011, he found himself in the final stages of an exit, with an $88m buyout offer in his lap.

The deal looked like a win all around. Ben, 31 at the time, would walk away a rich man — and the VC firm would more than double its investment.

But at the last minute, the investor, who had veto power, axed the deal. “He told me to hold out for something bigger,” says Ben.

That “something” never came: Over the next few years, the company lost momentum. Growth began to stagnate. Ben’s co-founders jumped ship. And eventually, when it folded altogether, it sold for pennies on the dollar.

Ben’s story is one of many cautionary tales of VC funding gone awry.

The VC obsession

Today’s startups are fixated on fundraising — and it’s certainly there for the taking: Last year, VC funding hit a decade-long record-high of $84.2B in the US.

Companies that raise a ton of cash are seen, by default, as successful. It’s every entrepreneur’s dream to close a big round, get the customary TechCrunch write-up, and secure the support of an all-star investment team.

In theory, venture capitalists should provide the following:

- Cash (to facilitate faster growth)

- Validation (to attract talent and customers, get press)

- Guidance (advice, connections, resources)

But as Eric Paley, a managing partner at the seed-stage venture fund Founder Collective, says, venture capital can be a “toxic substance that destroys [startups].”

Why?

1. They take big bets, and want a big payoff

As Ben learned, VCs often aren’t satisfied with $10m, $25m, or $50m exits or IPOs: they operate on a “go big or go home” mentality — and they typically want to see an outcome well north of $100m.

Venture capitalists are highly selective, and it’s not uncommon for a partner to only invest in 2-3 companies per year. They look for startups with explosive growth potential that cater to multi-billion dollar markets. A company that sells for $50m (and nets them, say, 30%) has very little impact on their portfolio.

“Some VCs would rather run you into the ground trying to make you a unicorn than entertain an offer under $100m,” one disgruntled founder tells me.

Founders who raise VC often end up in a position where they have to reject an offer that would be great for them just because it doesn’t satisfy an investor’s grandiose return expectations.

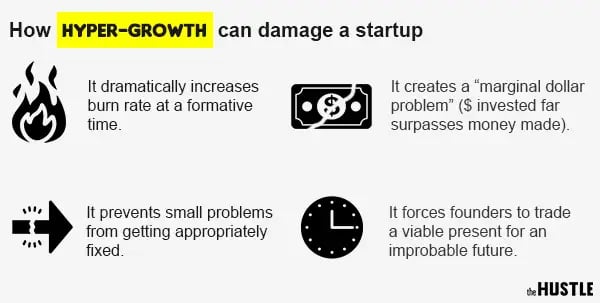

2. They push insanely fast growth at all costs

As Founder Collective investor Micah Rosenbloom says: “[VCs] are in the business of funding fast-growing companies” — not inventors or inventions. They often want to make you a “$100m company before you’re ready to be a $10m company.”

This “go big or go home” mentality can be incredibly damaging — and more often than not, it’s what Paley calls a “masked death spiral” for startups.

VCs want to see 10x to 30x returns, and they want to see them within a fund’s lifespan (6-8 years). This timeframe often forces companies to attempt to solve complex problems before they’re structurally ready to do so on a large scale.

But the biggest issue with this growth obsession is what Paley calls the “marginal dollar problem.”

“There is such a vanity rush toward revenue and growth, that people stop looking at what the cost of that revenue is,” he tells me. “They’ll do things like double the sales force when sales aren’t even close to returning on their expense. Soon, you’re spending $1 just to get back 50 cents.”

3. They severely dilute a founder’s stake in the company

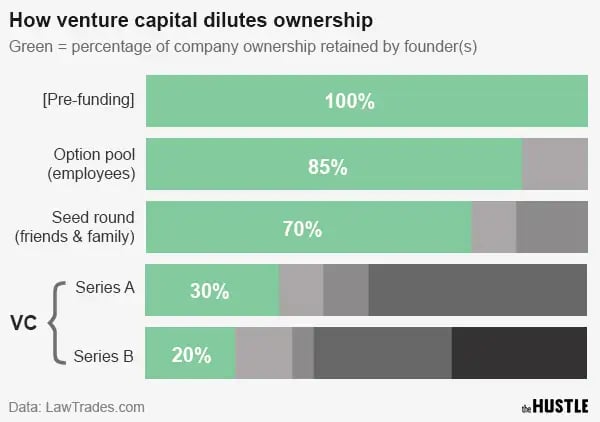

In the pursuit of capital, a founder relinquishes a hefty percentage of his or her company to investors.

During seed funding (family, friends, and angel investors), a company typically gives away about 15% of its shares. An option pool (giving shares to early employees) takes up an additional ~15%.

But things really start to dilute when VCs get involved. For the average Series A round, investors expect a 25% to 50% stake; for Series B, they expect around 33%. After a few rounds, a founder is considered lucky to be left with 20% of what he or she created.

These sacrifices should, in theory, give you a bigger payoff in the end — but that’s not necessarily true.

Take, for example, the case of Arianna Huffington (founder of The Huffington Post), and Michael Arrington (founder of TechCrunch).

Huffington sold her company for $315m, but multiple VC funding rounds left her with only a small percentage of the company. She walked away with a reported $21m. Arrington sold TechCrunch for ~$40m — one-tenth of Huffington’s exit — but since he didn’t raise external funding, his payday was around $25-30m.

4. Their advice and expertise is often overrated

There is a patently false understanding that venture capitalists have investment down to a science.

“Trust me, we have no idea what we’re doing sometimes,” an especially candid Silicon Valley VC tells me. “Like any financier, we rely on immeasurables like blind faith and intuition… There’s no fool-proof formula.”

Vinod Khosla, founder of Khosla Ventures, has said that most VCs “haven’t done sh*t” to help startups through difficult times, and he estimated that “70% to 80% percent [of VCs] add negative value to a startup in their advising.”

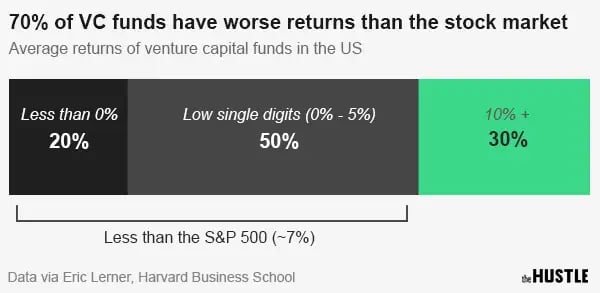

This is often coupled with poor outcomes: Research by Harvard lecturer Shikhar Ghosh indicates that around 75% of all VC-backed companies fail outright — and 95% don’t end up delivering projected return on investment. (VCs “bury their dead very quietly,” he told the WSJ).

A separate analysis revealed that more than 50% of all VC funds deliver low single-digit returns (worse than the S&P), and 1 in 5 funds actually manages to achieve an average return of less than 0%.

5. Raising tons of cash doesn’t = success

At some point, “valuation” (driven by inflated VC investments) became the barometer for success in the startup world.

But an in-depth analysis of 71 tech startup IPOs found that there is not a strong correlation between the amount of money a company raises and a successful outcome.

Consider this: 14 of the 20 startups with the largest market cap over the past 5 years raised $100m or less (compared to a $284m average); 6 of them (30%) raised less than $50m.

Founders are often tempted to raise 2 or 3 years of runway “just because they can.” This mentality can be a liability.

“The fact is that the amount of money startups raise… is inversely correlated with success,” says legendary VC Fred Wilson. “Yes, I mean that. Less money raised leads to more success. That is the data I stare at all the time.”

Venture capital is not inherently bad…

But in the current fundraising system, there is often a misalignment between what startups need and what VCs want.

For young startups, bootstrapping (funding a company out of pocket, and with the money generated from customers) is an ideal alternative: It enables founders to set their own pace and formulate their own concept of “value.”

But if you need outside capital, consider this rule of thumb: only raise enough to sustain operations for 18 months (plus/minus 25%).

And for the love of all that is holy, don’t waste it on ping pong tables, kombucha on tap, or branded trucker hats.