Most of us think about money constantly. Making it, saving it, spending, running out of it, and — if you’re lucky — retiring with it.

The only thing we think about just as much? How much other people have. Whether or not we admit it, we’re all at least a little curious.

We recently ran a survey on The Hustle, asking our readers everything from “How much money do you have in your checking account?” to “Are you stressed about money?” and received more than 3k responses. For this story, we filtered out 1,126 single-income earners and pulled together some of the most interesting takeaways.

Before we get into it, here’s a quick summary of some of our findings:

- Nearly 1 in 3 people have no idea how much they spend each month

- 50% of respondents are constantly ‘stressed’ about money — and this stress doesn’t decline until after people hit the $200k salary mark

- The majority of earners don’t make $100k until their late 30s or early 40s

- Only 14% of people have more than $50k in their checking/savings accounts; 25% have at least that much in stocks/mutual funds, and 34% in retirement funds

So, without further adieu, the million hundred-thousand-dollar question…

Are you making as much as your peers?

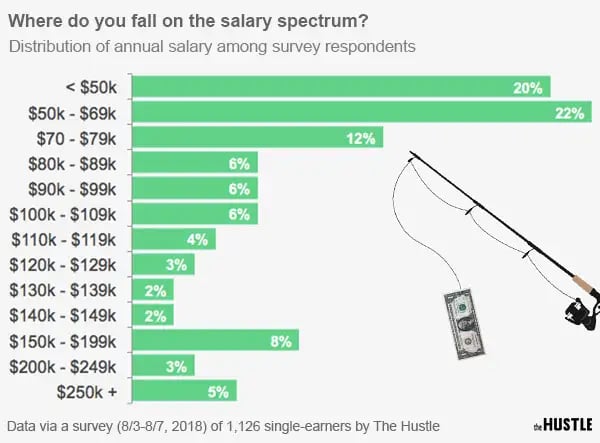

On the whole, our respondents averaged a self-reported $87k in annual income — nearly double the $44.5k national average according to the Bureau of Labor Statistics.

Our readers skew toward the ambitious, high performer type and work in competitive industries. But this figure was also impacted a bit by some outliers on the high-end; a closer look shows that 42% of our respondents make less than $70k.

Around 33% of folks meet or surpass the ever-desirable 6-figure mark.

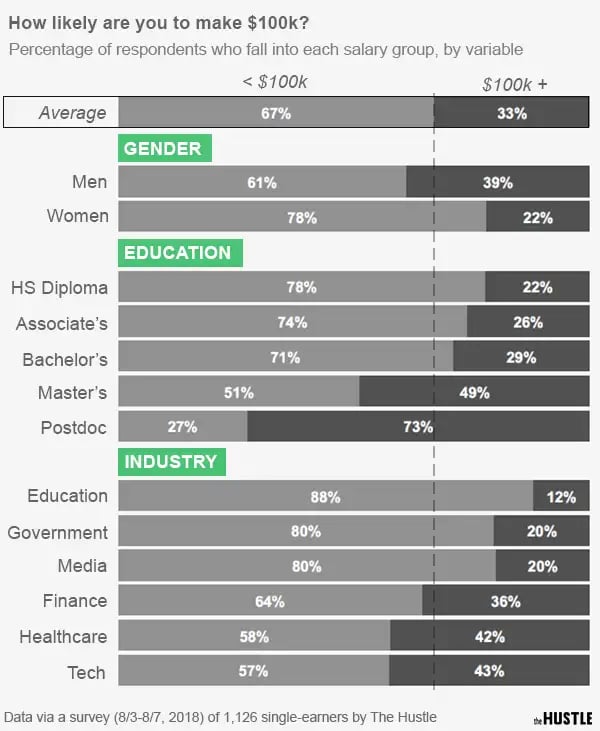

Not surprisingly, the chances of making a $100k+ salary vary greatly across a variety of data points, including gender, education level, and industry. We divided respondents into two groups (sub-$100k earners, and $100k+ earners), and took a closer look.

The contrast here is stark: 39% of men earn 6-figures (6% above the average), while just 22% of women do. As other studies have shown, the likelihood of earning a 6-figure salary also dramatically increases with educational attainment: 22% of our respondents with a high school degree made over $100k, compared to 73% of our postdoc respondents.

Industry appears to be the most impactful variable.

Depending on your profession, your chances of earning $100k vary from just 12% to 40%+. Educators, who are chronically underpaid, bottom out of list of lowest-paying professions, while tech workers top finance and healthcare employees for the #1 spot. On the whole, techies are nearly 4x as likely to make a 6-figure salary as teachers.

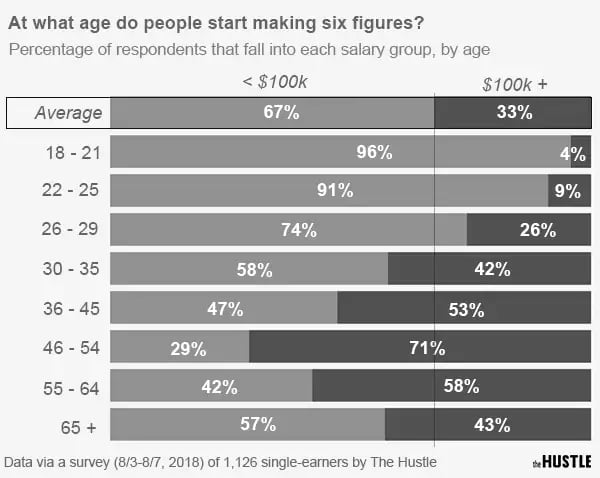

And how do you stack up with other people in your age group?

Only 13% of our respondents aged 25 or younger made 6-figures — but by the late 40s, 71% of people reported earning more than $100k. After the age of 55, salary growth chills a bit as people retire.

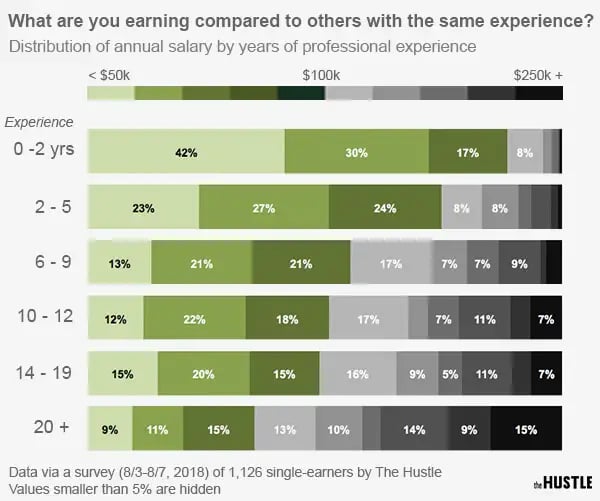

A final variable we looked at was experience: only 9% of workers with 2 years or less in the workforce make more than $100k — a figure that gradually increases with time.

Pro tip: For a quick ego boost (or reality check), use the graph above to see where your salary falls among your peers. For instance, if you’re making $100k 5 years into your career, congrats: you’re better off than 74% of your peers with the same experience.

Conversely, if you’ve been working for 15 years and you’re still under $50k per year, you’re being outpaced by 85% of the workforce.

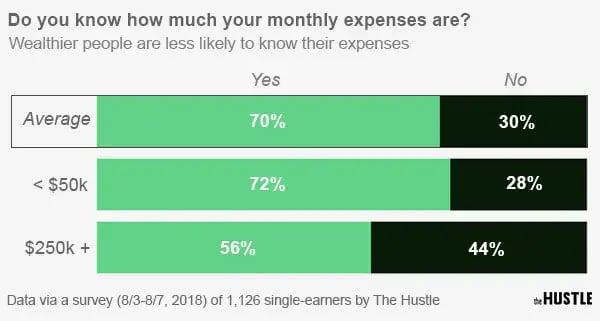

Once you get your paycheck, how do you spend it?

Turns out, only 70% of our answered ‘yes.’ This means that nearly 1 in 3 people, for one reason or another, have no idea how much they spend every month.

This percentage increases among higher earners: about 56% of $250k+ earners don’t know their monthly expenses. Most likely, this is because people with higher salaries tend to have other people manage their money. That, or rich people just don’t give a damn.

On the flip side, people with fewer assets tend to have a closer relationship with their money. Though we found it rather surprising that 28% of people making less than $50k still have their heads in the sand when it comes to their spending.

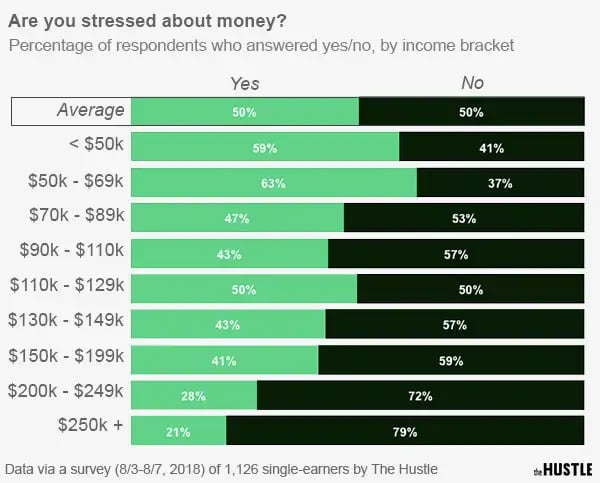

But just because wealthier people are less aware of their expenses doesn’t mean they’re stress-free when it comes to cash.

Overall, our respondents were split 50-50 on the question ‘Are you stressed about money?’ And as you can see below, stress levels linger far into the 6-figures.

People on the lower end of the earning spectrum are more likely to be stressed about money — but the figures don’t decrease much as we move up: by $199k, 40%+ of earners still grapple with money stress. Hell, even 21% of folks making $250k+ can’t relax. As we sometimes say around the office, more money, still problems.

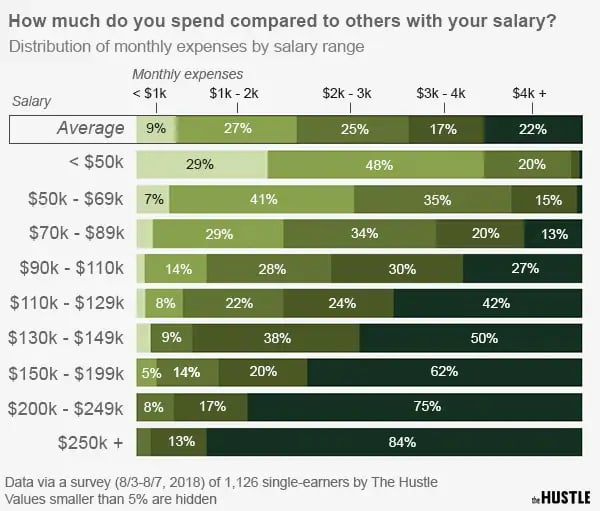

Using data from those who did know their monthly expenses, we were curious to see how these expenses varied across income ranges.

Unsurprisingly, as people make more, they spend more. But, there seems to be an “uncanny valley” between $90k and $110k where respondents were equally likely to spend $2-3k as they were $3-4k and $4k+.

In other words, at the 6-figure mark, people are equally likely to continue living frugally as they are to upgrade their lifestyle. It’s also possible that this is when single-earners have kids (the estimated cost of raising a child through age 17 is about $14k annually, or $1.2k a month).

In our sample, only 9% of people reported expenses of less than $1k per month. The majority (52%) fell somewhere between $1k and $3k, with significant patches at $3k-$4k (17%), and $4k+ (22%).

The percentage of $4k+ spenders increases dramatically with income bracket, while the other expenditure ranges remain fairly static. Of course, $4k+ is comparatively less for someone earning over $250k (about 1.6% of their earnings) than $2k is for someone earning less than $50k (about 4%).

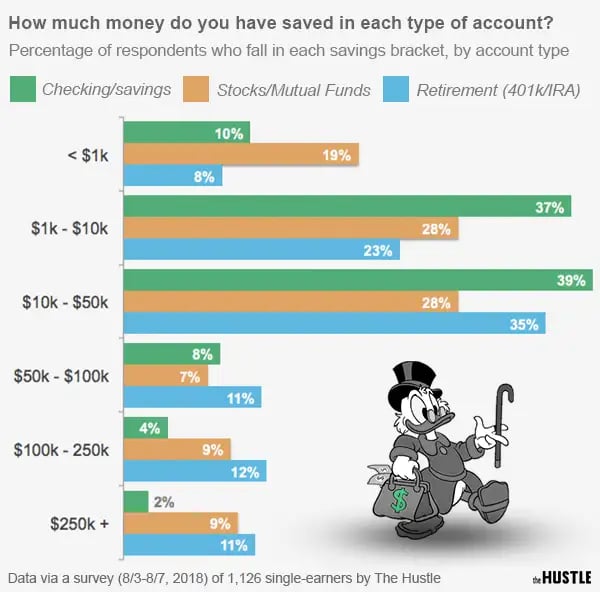

How do your savings stack up?

When all’s said and done — when the money’s in the bank and expenses are paid off — how do people invest what’s left?

We asked respondents to tell us how much they had invested in checking/savings accounts, retirement funds (like a 401k), and stocks/mutual funds.

Pop culture often depicts a “Scrooge McDuck” stereotype of wealth (ie. hoarding piles of cash and gold in massive vaults). But the reality is that a checking/savings account is arguably the worst place to park your money long-term.

For the most part, people seem to know this: regardless of how much they’re making, very few respondents (14%) have over $50k in their checking/savings.

Higher-earning liquid investments (like stocks, mutual funds, and exchange-traded funds) are a more popular choice: 25% report having at least $50k invested in stocks, compared to the 14% who have $50k or more in their checking accounts.

But retirement fund investments, like a 401k or IRA, skew the highest, on average. Here, 34% of respondents have at least $50k socked away — and nearly one-quarter have more than $100k. (Among people under the age of 35, these figures drop to 15% and 7%, respectively.)

This brings us to the crown jewel of money management questions…

What do wealthy people know that I don’t?

To close out, we asked some of our more successful respondents to list some of the investment and money management advice they wish they knew when they were younger. Some of our favorites:

- “Don’t save your credit card info online. That extra step of having to go get and enter your credit card for payment will save you from a lot of impulse purchases.”

- “You get paid what you ask for, not what you’re worth… Know your worth and fight for it. Don’t be afraid to ask for a raise.”

- “Put at least 10% of each paycheck towards building an emergency savings account with 6 months salary. This takes so much stress out of your life!”

- “Set up autopay for bills AND 401k/IRA so they’re out of sight, out of mind. Don’t give yourself the chance to pay a bill late or talk yourself out of contributing to retirement.”

- “Money management is less about the nuts and bolts of a budget, and more about defining your goals so you feel empowered in saving for what you need and comfortable in spending on what you prioritize.”

- “Compensation isn’t just your salary: It’s also travel stipends, insurance, vacation days, equity, bonuses, and 401(k) matching. You can negotiate all of them.”

- “So much of money management is psychological. Recognize that money is a tool to reach your own financial goals (and not others’). Learn about what options are available, and don’t let the fear of what you don’t know let you miss out on opportunities to earn, save, invest, etc.”

- “Don’t try to ‘Keep up with Joneses’. Odds are the Joneses are broke”

A note on methodology: The data in this story was collected between 8/3 and 8/7 of 2018, via an email survey sent out to readers of The Hustle.

Questions about our data, or just want to know more? Email us @ news@thehustle.co, or reply to this email. This report only scratches the surface of our findings.